Discussions often take longer than necessary, because people use the same term but seem to understand it differently. This also applies to central bank digital currency (CBDC). Some see CBDC as a preparation for a cashless society, a kind of European version of the ‘Chipknip’ (a now obsolete Dutch e-money product), while others see CBDC as a safe haven during an impending financial crisis. However, the implications for the economy of the various types of CBDC are radically different.

Let me start with the ‘Chipknip’ vision. The aim of preparing for a cashless society is to be able to cope smoothly with the decline in the circulation of banknotes with a digital product that is just as good or even better than the banknote. CBDC is suitable for this because it offers electronic value transfer that is available anywhere, anytime, change is not needed and that is cheap in comparison with the costs of the banknote chain.

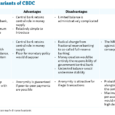

A bottleneck in this respect is the good protection of the privacy of banknotes. This form of CBDC should therefore be provided with an anonymous variant with a good encryption method from start to finish so that the intermediary (central bank or commercial bank) does not have access to it. Technically, this can be done with, for example, the blind signature of David Chaum. But this privacy protection should also have a limit: if certain payments are suspected of fraud or other criminal activities, investigative authorities should have access to it, accompanied by judicial guarantees. Furthermore, it is obvious that no interest should be paid on this form of CBDC and that a relatively low maximum limit should be set for the anonymous variant.

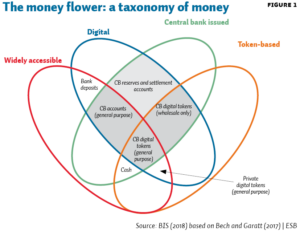

In essence, this form of CBDC is comparable to electronic money as referred to in the Electronic Money Directive, but with the European Central Bank and/or euro area national central banks as the issuer. The commercial banking sector can do this and offer the consumer a separate ‘Chipknip app’ on the mobile phone or as part of their own mobile banking app. In this case, the CBDC must be legally and operationally separate from the same consumer’s deposits with his own bank. Schematically, this form of CBDC can be represented as a five-corner model (figure 1a).

In the event of gradual introduction (e.g. with a low upper limit that is raised in steps), the monetary and financial stability implications will be relatively small. This seems technically, legally and project-wise feasible over the next five years. I would not be surprised if the Swedish Central Bank implemented such a model as e-krona.

A completely different goal of CBDC is to respond to concerns about the role of banks in the crisis and the continuity of payment systems (such as the recommendation in WRR, 2019). CBDC is suitable for this, because settlement bank risk is very small (in the case of CBDC, this is the probability that the central bank will go bankrupt).

The most far-reaching elaboration of CBDC for this purpose is the three-corner model in which every citizen can download an app with an unlimited CBDC option. As can be seen from figure 1b, the commercial banking sector no longer appears in this model. The figure is deceptively simple, but the implications of this variant for monetary policy and financial stability are so large and far-reaching that this option must be considered too risky (Metzemakers, in this ESB).

In order to reduce the confusion of words, it therefore seems useful to me to reserve the term CBDC for the variant with the aim of ‘preparing for a cashless society’. Assume that introduction will take place on a European scale (a Dutch solo project is not logical). And don’t wait until the use of cash has decreased: introduce CBDC much earlier so that everyone can get used to it at his or her own pace.

Literatuur

Berndsen, R. (2018) Financial market infrastructures and payments. Tilburg, www.warehousemetaphor.com.

Metzemakers, P. (2019) Veiliger geld kan tot hogere kans op bank-run leiden. ESB 104(4774), 254–255.

WRR (2019) Geld en schuld: de publieke rol van banken. Available at www.wrr.nl.