Following other countries, a debate on central bank digital currency (CBDC) has started in the Netherlands as progressive digitisation is bringing introduction within reach. The Netherlands Bank (DNB) participates in this debate with a critical attitude: do the potential benefits truly outweigh the risks and could these not also be achieved within the confines of existing financial structures?

In brief

– The introduction of this new type of money has benefits, but could fundamentally change the structure of the financial system.

– The risks it poses to the stability of the financial system can be overcome, but not without limiting the benefits.

– Introducing CBDC therefore requires careful consideration.

The issuance of CBDC would broaden access to digital central bank money to the general public. This type of money may be provided in the form of transferable digital credits (so-called ‘tokens’) or conventional accounts at the central bank. Currently, access to digital central bank money is limited to banks and a select group of public authorities, foreign central banks, supranational institutions and market infrastructure providers.

In the Netherlands, the discussion on CBDC is mainly driven by a desire to provide risk-free money in digital form to citizens while imposing market discipline on banks (Buitink and Van der Linde, 2019; Van der Linden, 2019). Moreover, it is argued that CBDC may contribute to financial stability by offering a resilient payment infrastructure (Van Tilburg, 2019). In the international discussion, other considerations dominate. In Sweden, people consider CBDC as a natural successor to cash, which is rapidly disappearing from circulation as payments progressively digitise (Sveriges Riksbank, 2018). In that context, CBDC would also maintain a direct link between citizens and the central bank. This link contributes to the public’s understanding of the role of central banks and the importance of their independence (Mersch, 2017).

Apart from these considerations, U.S. economists have proposed CBDC as a way to make phasing out cash acceptable to the public, which they consider desirable (Goodfriend, 2016; Rogoff, 2016). A discontinuation of cash would alleviate the effective lower bound (ELB) for policy rates and prevent illicit use of central bank money. In addition to a CBDC variant for the general public, calls have also been made for a variant aimed at non-bank institutions in wholesale financial markets (Box 1). The wholesale variant may make both clearing and settlement of securities and cross-border payments more efficient and would strengthen the transmission of monetary policy (Coeuré and Loh, 2018; Meaning et al., 2018).

Box 1 – Forms of money

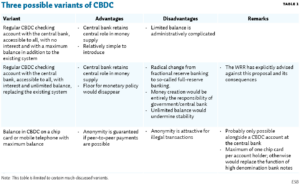

The money flower developed by the Bank for International Settlements (Bech and Garratt, 2017) provides an illustrative classification of money based on four characteristics:

– its form: digital or physical;

– the issuer: a central bank or other;

– accessibility: wide or restricted;

– technology: token or account-based (the former allows for transactions outside of central bank’s ledger, the latter does not).

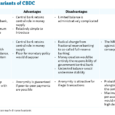

CBDC differs from cash by its digital form and from conventional central bank reserves by its wider accessibility. Three forms of CBDC can be distinguished, depending on the accessibility and technology.

Threshold for introducing CBDC is high Introducing CBDC requires careful consideration because of the potential far-reaching implications for our well-functioning financial system (BIS, 2018). Traditionally, central banks restrict access for non-banks to limit their footprint in the financial system and foster the role of market forces. When credit decisions are in private hands, efficient use is made of society’s decentralised knowledge (Hayek, 1945). Public safeguards in the form of banking supervision, deposit insurance and central banks’ lender-of-last-resort (LOLR) operations keep commercial banks’ deposit base stable, enabling them to provide welfare-enhancing maturity, liquidity and credit risk transformation. In addition, limited access to digital central bank money, low denominations of banknotes, the inconvenience of cash for large value storage and payments ensure that banks’ deposit base cannot suddenly flow to the central bank in turbulent times. Within this context, central banks steer overall financial conditions through monetary policy, keeping inflation in line with their price stability mandates. In sum, our monetary system is built on strong logical foundations – market functioning within public safeguards – and has served us well (Jordan, 2018). The Netherlands Bank therefore has a critical attitude towards introducing CBDC (DNB, 2018).

Benefits cited are not undisputed

While the status quo should not be changed hastily, the digitisation of payments, changed views on the desirability of central bank intermediation and the rise of crypto-assets do provide a rationale for investigating CBDC. In doing so, the underlying arguments need to be understood and carefully weighed against the implications for the stability of the financial system.

There are several caveats to the arguments in favour of issuing CBDC. Starting with the argument that CBDC would provide risk-free money in digital form to citizens while imposing market discipline on banks. It fails to mention that the Deposit Guarantee Scheme already provides EUR 100,000 euros per bank of risk-free money in digital form to each citizen. Moreover, using depositors as a disciplining mechanism is not efficient. Small depositors bear little credit risk as they have a relatively senior claim on their bank. Due to the buffer role of equity and subordinated debt, depositors are inherently insensitive to incoming economic and bank-specific news (Holmstrom, 2015). Within this context, the Deposit Guarantee Scheme prevents unwarranted herd behaviour among depositors (Diamond and Dybvig, 1983). In contrast to depositors, bank equity and subordinated debt holders have a strong financial incentive to monitor banks – particularly given the bail-in mechanisms introduced in Europe after the Great Financing Crisis.

Furthermore, despite the presence of the Deposit Guarantee Scheme, banks are exposed to competition within the broader financial sector. On the asset side, for example, Dutch banks have lost a five percent share of the mortgage market to pension funds and insurance companies over the past years (DNB, 2016). This indicates that the competition arguments in favour of CBDC is not compelling. On the liability side, depositors can also hold financial wealth through money market funds. However, in the Netherlands, there is limited demand for money market funds that invest exclusively in government bonds. This raises the question whether there is a genuine demand for risk-free money in digital form beyond the scope of the Deposit Guarantee Scheme.

The arguments put forward in favour of CBDC in the international debate not have escaped criticism (Akerboom et al., 2018). For example, the disappearance of cash – as may happen in Sweden – does not automatically make CBDC necessary or desirable. Monetary policy can be effective even without cash (Woodford, 2000), while innovation and efficiency in payments generally originate from private initiatives (Boonstra, 2019) – recently mostly outside the traditional banking sector.

The proposal to phase out cash in order to eliminate the ELB has also been criticised. For example, deep-negative interest rates may provoke non-linear effects. Nor is it immediately obvious that monetary transmission needs to be strengthened, both with respect to savings and money market interest rates (BIS, 2018; Potter, 2017).

It is also not self-evident that anonymous payments should be abolished to prevent illicit payments (Mersch, 2017). Finally, a forced digitisation of payments may exclude some parts of society (such as the elderly, digitally illiterate and visually impaired) and increase the vulnerability of our payments system to digital interruptions

Important choices in case of eventual introduction

Introducing CBDC would create considerable risks. Frequently mentioned is the risk of digital runs to the central bank. In this sense, cash and CBDC are not substitutes. After all, CBDC is superior in terms of the traditional functions of money as a means of payments and store of value. But even in quiet times CBDC would have implications for the structure of the financial system. A portion of the digital part of the money supply would migrate to the central bank balance sheet. Commercial banks’ deposit base would shrink and become less stable, while the central bank would be forced to take more maturity, liquidity and credit risk. This may reduce the efficiency of the overall financial system.

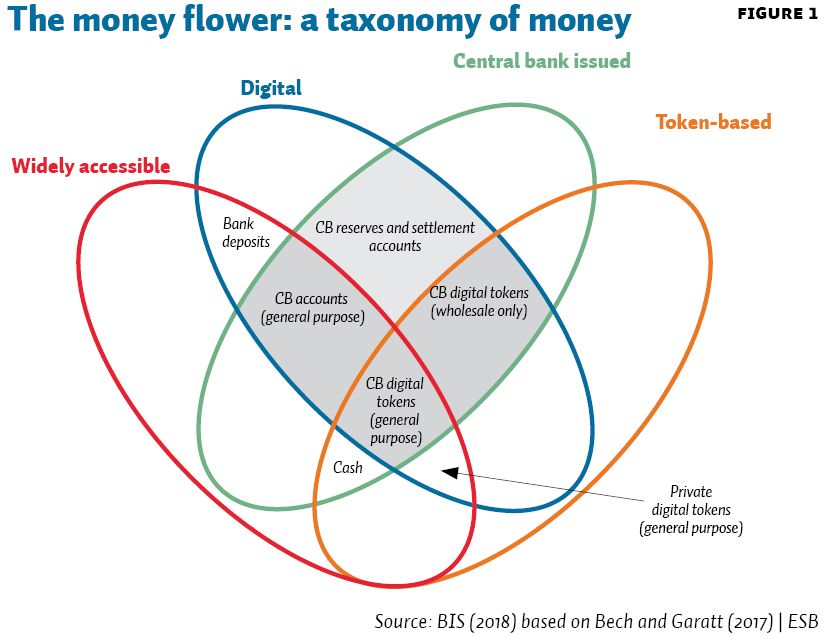

An open question is whether these risks can be mitigated through the CBDC’s design. The modalities may vary in terms of access, remuneration, upper limits, opening hours and anonymity (Figure 2). For example, the potential demand for CBDC may be dampened by applying substantially lower rates or an upper limit at, for example, EUR 100,000 like under the Deposit Guarantee Scheme. Doing so would limit the flow of funds to the central bank. However, these modalities carry new complexities: in the current interest rate environment, applying substantially lower rates beyond a certain amount would imply highly negative rates, and applying an upper limit would exclude the possibility to have anonymous CBDC. Generally speaking, the substitution effects vis-à-vis banknotes and commercial banks deposits will be smaller for the modalities on the left in Figure 2. However, particularly in turbulent times, the central bank may come under public pressure to relax these modalities.

Conclusion

The ongoing digitisation of payments raises the question of whether central banks should provide digital money to the general public. The advantages of CBDC are subject to debate and need to be carefully weighed against the disadvantages and risks. Both the advantages and disadvantages are multifaceted and strongly depend on the chosen variant. The technology is still evolving. It is clear that central bank digital currency may have far-reaching consequences for the structure and dynamics of the financial system. Many of the benefits aimed could also be realised within the existing confines of the financial system. Introducing central bank digital currency thus requires careful consideration.

References

Akerboom, S., A. Houben en D. Reijnders (2018) Central bank digital currencies: alternatives, benefits and risks. Bančni vestnik/The Journal for Money and Banking, 67(11), 61–65.

Bech, M. en R. Garratt (2017) Central bank cryptocurrencies. BIS Quarterly Review, September, 55–70.

BIS (2018) Central bank digital currencies, March. Bank for International Settlements, Committee on Payments and Market Infrastructures. Article at www.bis.org.

Boonstra, W. (2019) Publieke geldschepping kent belangrijke nadelen. ESB, 104(4769), 32–34.

Buitink, P. en R. van der Linde (2019) De econoom aan zet voor bankrekening zonder kredietrisico. ESB, 104(4769), 21–23.

Cœuré, B. en J. Loh (2018) Bitcoin not the answer to a cashless society. Opiniestuk Financial Times, March 13. Article at ecb.europa.eu.

Diamond, D.W. en P.H. Dybvig (1983) Bank runs, deposit insurance, and liquidity. The Journal of Political Economy, 91(3), 401–419.

DNB (2016) Kredietmarkten in beweging. De Nederlandsche Bank.

DNB (2018) Visie op betalen 2018–2021. De Nederlandsche Bank.

Goodfriend, M. (2016) The case for unencumbering interest rate policy at the zero bound. Discussion article for the Economic Policy Symposium at Jackson Hole. Available at www.cmu.edu.

Hayek, F. (1945) The use of knowledge in society. The American Economic Review, 35(4), 519–530.

Holmstrom, B. (2015) Understanding the role of debt in the financial system. BIS Working Paper, 479.

Jordan, T.J. (2018) How money is created by the central bank and the banking system. Presentation at the Zürcher Volkswirtschaftliche Gesellschaft. 16 January, Zürich.

Linden, M. van der (2019) Tijd voor transitie van financieel-monetair systeem naar digitaal tijdperk. ESB, 104(4769), 24–27.

Meaning, J., B. Dyson, J. Barker en E. Clayton (2018) Broadening narrow money: monetary policy with a central bank digital currency. Bank of England, Staff Working Paper, 724.

Mersch, Y. (2017) Why Europe still needs cash. Article at www.project-syndicate.org.

Potter, S. (2017) Money markets at crossroads: policy implementation in times of structural changes. Presentation at the University of California. April 5, Los Angeles. Available at www.newyorkfed.org.

Rogoff, K.S. (2016) The curse of cash. Princeton: Princeton University Press.

Sveriges Riksbank (2018) E-krona project, report 2. Sveriges Riksbank. Report available at www.riksbank.se.

Tilburg, R. van (2019) Stabiliteit door Revolutie. ESB, 104(4769), 35.

Woodford, M. (2000) Monetary policy in a world without money. International Finance, 3(2), 229–260.